While the scam is over, the story behind it is not. That won't change as long as it's main character remains in hiding.

The dollar amount allegedly stolen by 'Crypto Queen' Ruja Ignatova is approximately the same amount Bankman-Fried is accused of losing. But Sam's story is downright boring compared with the chaos still happening today in the aftermath of OneCoin.

Both Sam and Ruja are accused of losing $3 - $4 billion of their user's funds, which puts them in a category beyond just running "crypto scams"- they're officially among the "largest scams ever" both in the number of victims, over 3 million, and the total dollar amount taken from them - over $4 billion in USD value, according to the FBI and Europol.

First Time Hearing About This?

The first time I heard of "OneCoin" it was already over, they had just been shut down, and the people behind it were in the process of being tracked down and arrested.

I was shocked - how could a multi-billion dollar crypto scam happen and it wasn't even on my radar?!

Good news, the problem isn't that you weren't paying attention - OneCoin deliberately avoided attracting attention from people in select 'Western' nations. They feared that law enforcement in these countries were tech savvy, and way ahead when it comes to cases involving crypto.

Still, today it's not uncommon to find someone who is in the crypto industry (full time) who says they've never heard of OneCoin. But most common seems to be someone remembering OneCoin was 'some kind of scam a few years back' with maybe 10% of people aware of its size - one of the largest scams in history and on the extremely short list of scams with a multi-billion dollar price tag.

It was the US FBI they feared the most, and to avoid them they also avoided scamming US citizens. They believed this was so important that if someone in the US ended up on their site and wanted to join - the signup page would give them an error and close itself.

Ironically, the FBI is leading the way in dismantling OneCoin, and is credited with tracking down many of the executives in custody today.

Comparing Sam and Ruja May Be Unfair... to Sam. He Isn't Nearly as Evil...

There's one huge difference between them - Sam started a legitimate business. The more money he had the more careless he became. But those funds were handed over to him for use in his legitimate business, which did exist..

Ruja never intended to start a business - she created a scam. 'OneCoin' was a fraud from the first day it launched, not a single feature ended up to be true.

Her public image was the same, professionally she introduced herself as "Dr Ruja Ignatova" and claimed an educational history of elite colleges, and an employment history at major financial firms.

She is the definition of 'scammer' - so dedicated to it she lives her daily life as the character she created for the single purpose of getting people to believe the opposite of what is really happening.

|

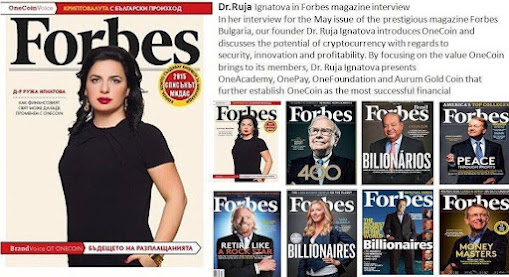

| Exactly how it appeared on OneCoin's website - but when Forbes was contacted they said OneCoin simply purchased as space, in that space they put an interview, then announced people could read an interview with Ruja in the latest edition of Forbes Magazine. |

People behind scams this large don't struggle morally about what they're doing, far from it. They become addicted to the power they feel whenever they step on stage and see thousands of people clapping and cheering for them - the same people they will soon financially ruin. In these short moments they feel like the smartest person on the planet.

What Puts This Story On a New Level of CRAZY: OneCoin Wasn't Even Real...

To be clear, I am not saying "her coin wasn't as good as she claimed" - I'm saying they didn't even have a coin.

She nicknamed their non-existent cryptocurrency the "Bitcoin Killer', claiming the blockchain technology behind it was so superior, it would soon come to replace Bitcoin. In reality, she had nothing. No blockchain, no cryptocurrency.

What they did have was the OneCoin App, where people couduse real money to purchase OneCoin, and see it added to their balance - that's the entire system.

The price of OneCoin was also entirely imaginary, having nothing to do with supply and demand they could simply decide what the app would show the public, and of course, they decided to make it look like demand was huge.

In e-mails obtained by investigators and used in court against OneCoin leaders, Ruja is seen telling the developers building the OneCoin system that:

"We would like to be able to set the price manually and automatically and also control the traded volume."

Legitimate cryptocurrencies cannot control any of those - the market decides the price, and volume is simply the total amount people bought or sold.

Now That They at Least Appeared to Be Having a Strong Start, They Would Use Their Fake Coin's Fake Success, to Bring in Real Money...

Within the app was also the only 'exchange' where OneCoin could be traded - it had to be this way because trading it anywhere outside of their app would have been technically impossible - no transferable cryptocurrency existed. But according to their app, their imaginary cryptocurrency was quickly increasing in value, and that's all they needed to keep users buying more and telling their friends.

This is where the pyramid aspect comes in to play -users would receive commission from people they invited to OneCoin, then they would also receive commission if that friend brought their friends.

OneCoin users who referred a lot of other users are the only group of people who walked away with a profit, but it's impossible to figure out who was knowingly promoting a scam, and who was a victim believing they were sharing something good.

OneCoin Held 'Conferences' Attended By Thousands - Here Ruja Would Speak About Blockchain Revolutionizing the World of Finance...

Always booked as the special 'keynote speaker' at her own events, Ruja would give long speeches about what blockchain tech can do, and will do in the future. But back in reality, no blockchain of any kind was being used at OneCoin.

OneCoin's final event before it all came crashing down, the 'Crypto Queen' makes a dramatic entrance - pyrotechnics included.

E-Mails obtained by investigators and shown in trials of her partners made it clear - she was the mastermind behind the lies, fully aware of every shady thing they were doing.

In one exchange with co-founder Karl Greenwood, she says

“We are not mining actually – but telling people shit" and jokingly referred to OneCoin as '

Trash Coins'.

The Collapse...The red flags started to pile up - people discovered that some of OneCoin's directors had previously been involved in other known scams.

Plus, for years people requested any verifiable evidence for any of their claims, and the excuses dragged on so long it became obvious they were hiding something. They had been telling so many lies for so long that their own statements would occasionally contradict things they said in the past.

As the inflow of money began to slow down, use of their fake exchange became limited, dividing their members into different levels with each given different trading restrictions. Those who spent a lot on 'educational materials' could trade on more days than those who didn't.

They were making it impossible for there to be a run of users withdrawing until there was nothing left.

As OneCoin Comes Crashing Down, Ruja is Nowhere To Be Found...

Some believe she bribed government officials in the 3 countries she had homes in, so they would agree to warn her in advance of any plans against her, or her business.

While that hasn't been proven, we can say that somehow she managed to stay months ahead of authorities, and was long gone when the day came, and OneCoin was forced to shut down as it's leaders were rounded up and arrested.

In those final months without Ruja, OneCoin stayed open for business, with her younger brother Konstantin Ignatov taking over the title of CEO. But his reign as OneCoin's top boss was a short one, as he was arrested March 2019 in Los Angeles, and it all ending with him pleading guilty to fraud and money laundering charges.

Co-Founder Greenwood was detained in Thailand in 2018 and then extradited to the United States - just 3 weeks ago his case was closed after a deal to plead guilty was reached. He still faces up to 40 years in prison.

Mark Scott, a former corporate lawyer, was convicted in November 2019 of laundering $400 million for the group by using a network of shell companies, offshore bank accounts and investment funds.

Another man, David Pike, pleaded guilty to committing bank fraud. He was sentenced to two years probation in March.

Not Even her Husband or 9 Year Old Daughter Has Heard from Her Since...

Most shockingly, she left her husband and now 9 year old daughter behind as well.

They are said to be under 'constant surveillance' as authorities were expecting Ruja to eventually make contact with them. If she has, it was done without anyone noticing, as the official status of her with the FBI describes her 2019 disappearance has the 'last time anyone has heard from or seen' her.

Is She Now a He?

It's hard to believe that a 3 year long global search with the powers of multiple law enforcement agencies from multiple countries behind it still hasn't found anything - to avoid even the occasional random sighting she either never goes outside, or has drastically changed her appearance.

One way people believe she could do this would be for her to live as a man.

|

| A professional sketch artists rendering of Ruja as a male, commissioned as part of Tradingpedia's research in to her disappearance. |

Simpler methods of disguise have been suggested too, such as plastic surgery to make her face and body thinner, along with dying her hair blonde, would probably also make her unrecognizable.

Possible Leads...So where is Ruja Ignatova now? On a recent BBC podcast, Jamie Bartlett suggests that Ruja may be living in luxury in Dubai. This revelation comes after reports of her being spotted in Southeast Asia, specifically in Thailand.

According to documents obtained by the BBC, Ignatova allegedly worked with Sheikh Faisal bin Sultan Al Qassimi, a royal in the United Arab Emirates, to release funds that had been frozen over suspicion of money laundering. Furthermore, it is believed that she purchased a $20 million villa in the UAE, which may serve as her hiding spot for the past five years.

The investigation also uncovered a mega-million deal struck between Ignatova and Emirati royal Sheikh Saoud bin Faisal Al Qassimi, a known enthusiast of cryptocurrency. In 2015, Al Qassimi reportedly sold 230,000 Bitcoins worth more than $48 million to Ignatova.

As mentioned when talking about her initial disappearance, many speculate that Ignatova may be buying intel and bribing authorities wherever she is, which would explain her ability to evade investigators for so long.

That is The Cliffhanger Ending to The Story So Far...If this is beginning to feel like a movie, you're not too far off - because the story will soon become a TV docuseries, according to entertainment news site

Deadline.

We Want To Hear from YOU! Tell us your thoughts:

Who do you think is WORSE?! Sam, or Ruja? + Share how you decided.

Tweet us @TheCryptoPress

-----------

Author: Ross Davis

Silicon Valley Newsroom

GCP | Breaking Crypto News